Read our update to understand how the coronavirus pandemic is impacting the UK and global economies.

The COVID-19 crisis presents a unique challenge for the UK and global economy, as it constitutes a massive, simultaneous shock to demand, supply, and financial markets. Consumer demand has dropped sharply due to social distancing measures and widespread business closures, while production has fallen due to supply chain disruption and firms reducing operations. These impacts have, consequently, been amplified by decreased household and business confidence, in addition to a tightening in financial conditions.

Since the beginning of the outbreak, the CBI Economics team has been compiling thousands of anecdotes from businesses across the country to track the impact of the outbreak. The CBI’s regular sectoral surveys have also started including special COVID-19 questions to quantify the outbreak’s effect on activity. As a result of this intelligence-gathering, the CBI has been able to work closely with the UK government to help businesses overcome the challenges they face. View the CBI’s breakdown of financial support available for more information on those schemes.

What was the economic impact of COVID-19 in Q1 2020?

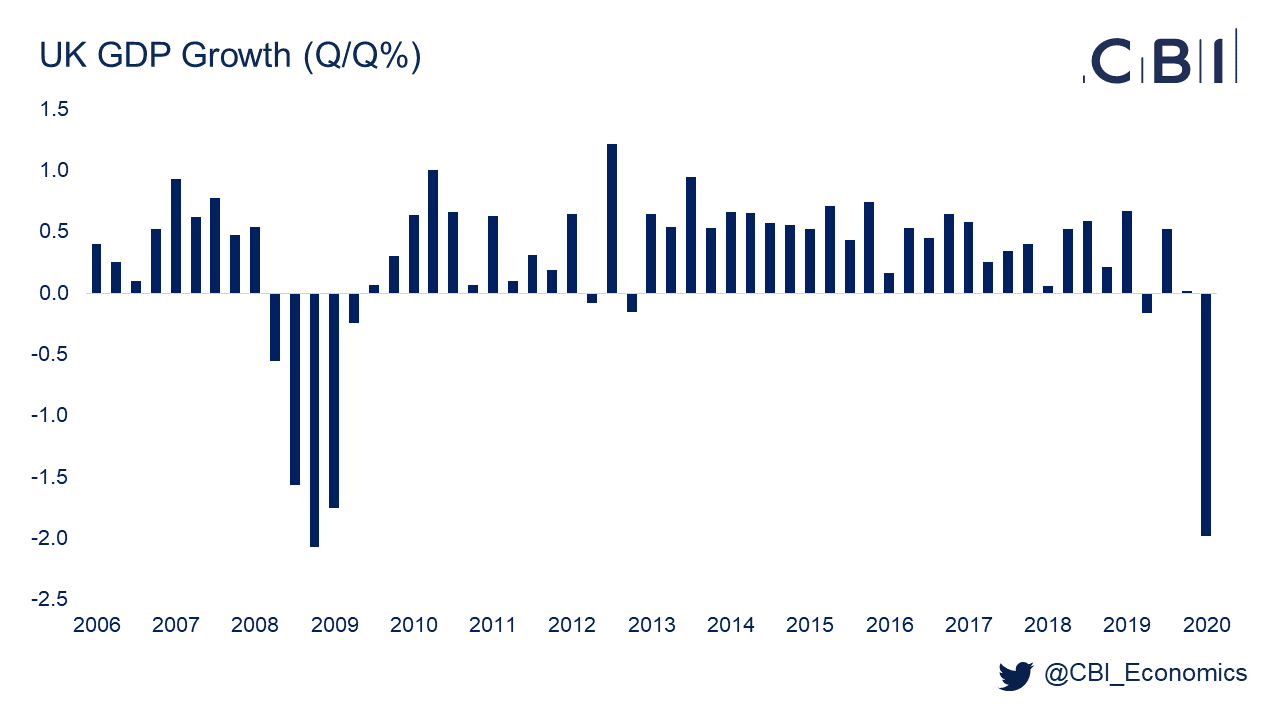

The scale of the hit to economic activity was made clear in the Office for National Statistics’ (ONS) first estimate of GDP in Q1 2020, which reported that output fell by -2.0% (from 0.0% in Q4 2019). This constituted the fastest quarterly fall in GDP since the depths of the financial crisis (Q4 2008).

The fall in quarterly GDP was driven by a sharp monthly decline in output of -5.8% in March, marking the fastest month-on-month contraction in GDP since this series began in 1997. This, naturally, reflected social distancing measures implemented at the end of the month.

The impact of the crisis was evident in the fastest quarterly fall in consumer spending (-1.7%) since 2008. Expenditure dropped sharply in those sectors that are most exposed to social distancing measures, such as restaurants, hotels, transport, and clothing. Meanwhile, there were some increases in spending on categories of goods such as food and drink, alcohol and tobacco, and recreational goods such as TVs.

Looking at the sectoral breakdown of GDP, services fell at its fastest quarter-on-quarter rate on record (-1.9%), largely due to sharp declines in the distribution, education, accommodation, and transport sectors. Industrial production (-2.1%) and construction (-2.6%) also saw substantial falls in output.

How does the hit to UK GDP in Q1 2020 compare with its international peers?

The global nature of the COVID-19 pandemic – currently affecting 216 countries, areas, or territories across the world – has resulted in widespread falls in GDP across nations. Advanced economies have been relatively more impacted compared to developing countries as containment measures have a disproportionate impact on services sectors (especially those that require social mobility, such as travel and hospitality). Countries across the globe have responded to the crisis with a wide range of fiscal and monetary policy measures, such as business loan schemes and bank rate cuts.

Looking at its G7 peers that have published Q1 2020 GDP figures, the UK had the third-slowest contraction in output in quarter-on-quarter terms. By comparison, Japan saw GDP fall by -0.9% in Q1 2020, the US by -1.2%, Germany by -2.2%, Canada by -2.6%, Italy by -4.7%, and France by -5.8%. Businesses should note that these widespread falls in GDP internationally will have a disproportionate impact on open economies where trade makes up a large share of national output, such as the UK.

What can we expect in Q2 2020?

The scale of the fall in GDP in Q1 2020 gives a glimpse into what will be an even deeper downturn in Q2 2020. Survey indicators, such as the CBI Growth Indicator and IHS Markit/CIPS PMIs, suggest that we may see the sharpest quarterly contraction in living memory. This is supported by recent ONS data on the business impact of COVID-19. Between 20 April to 3 May 2020, nearly a quarter of firms temporarily paused trading, while, of those companies that continued trading, three out of five firms reported that their turnover had decreased to some extent compared to normal.

However, the unprecedented nature of the crisis means that any estimates of how much UK GDP will fall by in Q2 are highly uncertain. The average of external forecasts sees GDP contracting by -12% quarter-on-quarter in Q2; however, these forecasts range from -3% to -24%. The Bank of England’s recent scenario, by comparison, expects GDP to decline by -25% in Q2 (following an expected fall of -3% in Q1).

What is the impact on the UK economic outlook?

As the UK begins to look towards restarting the economy, beginning with the latest government guidance announced on 10 May, it’s important to start to think what a recovery might look like.

The Bank of England’s latest Monetary Policy Report (MPR) set out an “illustrative scenario*” to estimate the economic impact of COVID-19 through 2022. Under this scenario, which assumes social distancing measures and government policies are unchanged in Q2 2020 and then loosened in Q3, GDP would fall by -14% year-on-year in 2020 before growing by 15% in 2021 and 3% in 2022. This is what economists sometimes refer to as a “V-shaped” recovery, where a sharp fall in output is followed by a rapid recovery.

However, households’ heightened uncertainty about the outlook, particularly with regards to job prospects, are likely to continue dampening spending after social distancing measures are lifted. As a result, consumption falls faster than incomes, leading to a degree of precautionary saving. Business investment is also anticipated to be constrained by elevated uncertainty, alongside tighter financial and credit conditions.

The MPR’s scenario expects that the sharp decline in oil prices this year, alongside weaker consumer demand, will slow inflation to around 0% at the end of 2020. However, inflation picks up again through 2022 as these factors unwind and domestic demand recovers.

Furthermore, in this scenario, the unemployment rate is assumed to rise to 9% in Q2 2020 but falls back gradually as the economy recovers (to 7% in 2021 and 4% in 2022). The Job Retention Scheme is expected to have reduced this peak significantly, which softens the longer-term impact on the UK’s labour supply.

The Bank of England also released an interim Financial Stability Report, which outlined the results of a “desktop stress test” to gauge the resilience of the financial system amidst the COVID-19 pandemic. The results of the test led the Financial Policy Committee’s to judge that major UK banks have sufficient capital buffers to withstand losses that would be expected under the MPR’s scenario, while still being able to provide credit to the economy.

What is our view going forward?

With the UK starting to move into the next phase of the crisis, whereby some sectors can gradually re-open, it will continue to be of paramount importance to understand how the shocks associated with COVID-19 develop across the economy.

The extent to which activity recovers will depend on the path of the outbreak and the subsequent duration of social distancing measures and government policy support. We will also need to consider how households and businesses respond to the ongoing uncertainty associated with the crisis, especially as voluntary social distancing may continue after official measures are eased.

The process of restarting the economy will be complex and gradual, but, in the end, supporting the health of the population will be the key to unlock the economy’s recovery.

What does this mean for UK businesses?

Businesses are currently living through the deepest, sharpest downturn in economic activity in modern history. We have yet to see the peak impact on activity in the economic data that is currently available.

The impact of the COVID-19 crisis varies by sector and across companies. Therefore, firms should be aware that some parts of their supply chain may be relatively more impacted than others.

In addition, the timing and nature of the recovery remains deeply uncertain. Much of the restart will depend on the pace at which both social distancing measures and government support schemes unwind, but firms should also consider the longer-term impact of businesses and households’ changing behaviour. As a result, firms should continually review their business planning, such as considering how they can operate while following social distancing rules.