Find out how CBI Economics helped Lloyds Banking Group to identify and assess high-value regional clusters.

In our new world of big data, advanced metrics and limitless information how do policymakers or investors identify and assess an industrial cluster? Not easily. Despite these advancements, frameworks to evaluate clustering have long been relatively primitive. Compound this with decades of debate on their definition, features and boundaries and economists are left without a tool that would be clearly fundamental to developing a robust industrial strategy.

In partnership with Lloyds Banking Group (LBG) and The Data City (TDC), CBI Economics have undertaken an exercise to understand the UK's high-value and emerging clusters.

Business clusters, anchored by world-class companies and institutions, are engines of growth and a driving force behind economic development. In the UK, policymakers have repeatedly recognised that clusters are key hubs of local economic activity and play a vital part in our economy. Clusters are centres of high-quality jobs that tend to pay well, bolster regional supply chains and attract further investment.

The project utilised TDC's Real-Time Industrial Classifications (RTICs), that go beyond the official, widely accepted Standard Industrial Classification framework, or SIC codes, that are seen as being inflexible to the emergence of new types of economic activity and technologies. RTICs, driven by web-scraped data on how companies classify themselves, offer a more-up-to-date perspective of the UK economy and allow for a focus on emerging and fast-growing areas of the economy such as Net Zero, Cyber and Advanced Manufacturing. At the time of this research, RTICs spanned 53 total sectors.

CBI Economics' report with LBG and TDC provides an in-depth analysis of the cluster economy in four major UK regions: the North West, the West Midlands, Yorkshire and the Humber and the North East. The research highlights the emerging and significant sectors driving economic growth in these areas, including particularly strong industries such as Net Zero, Life Sciences, Advanced Manufacturing and the Marine and Maritime sector. These sectors are identified as crucial contributors to the UK and regional economies, in terms of Gross Value Added (GVA), employment, productivity and investment.

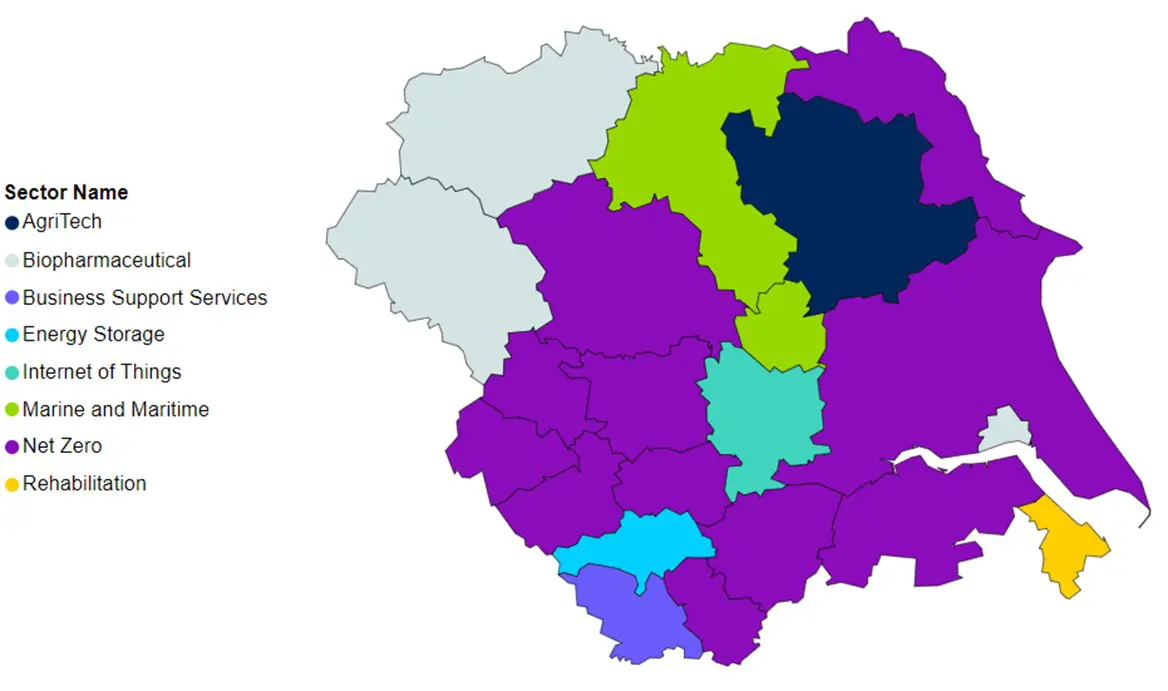

Figure 1 - Top cluster in each Local Authority District (LAD) in Yorkshire and the Humber

In producing this report, CBI Economics developed a thorough platform collating a series of metrics on almost 20,000 clusters across the UK. An iterative data collection, long-listing and short-listing process generated a suite of metrics by which to assess clusters, categorised into core and supplementary types. Core metrics cover the total number of businesses, employment, economic output, business location quotient, employment location quotient and labour productivity. These metrics were combined into an index, with equal weighting, which was used to rank UK clusters across local authorities and combined authorities. Whereas the supplementary metrics presented datapoints on topics such as business maturity, skills, innovation and investment and labour supply.

For example, some of the headlines we've drawn on the South West include:

- The South West hosts a very strong Net Zero sector and within this a thriving industry for Clean Technologies. Net Zero contributes £6.5 billion in GVA, 4.4% of the regional economy, and supports 66,000 FTE jobs. Thriving local Net Zero clusters were identified in Cornwall, Bristol, Wiltshire and Bournemouth.

- Energy Generation performs very well in the South West, as a total business population of 2,100 contributes £2.4bn in GVA and accommodates 25,800 FTE jobs.

- Notably, 10% of UK FoodTech GVA is generated in the SW and 10% of the UK's Quantum Economy and Software as a Service (SaaS) sector also originates within the SW.

- The West of England combined authority shows strong performance and clustering in FinTech and Life Sciences, that contribute £206m and £538m in GVA respectively.

- Other interesting clusters are Electronics Manufacturing (close to £1bn in GVA) and Photonics (a smaller, but more concentrated sector).

These metrics were the basis for selecting which clusters were carried forward into the cluster deep dives, some of which have been included in the final report. Deep dives reviewed and presented more qualitative information, to supplement the metrics, such as local investment prospectuses, local government reports and policy and also what businesses and education institutions had written about the area.

November 2024 saw the publication of the Industrial Strategy Green Paper which named eight growth driving sectors. Amongst these were advanced manufacturing, clean energy, life sciences and the creative industries which, at present, do not fit neatly into the Government's sectoral classifications. Our work with Lloyds Banking Group, using The Data City's platform, can fill this information gap and ensure policy and decision makers have the best tools available at their fingertips to capture, evidence and evaluate the high-value, emerging and significant clusters throughout the country that will be paramount to building a robust and reliable plan for growing the economy and unlocking investment.

About CBI Economics:

CBI Economics is the economic consultancy division of the CBI. We offer a suite of services including bespoke economic analysis and business surveys. With unrivalled policy knowledge and business insights combined with economic expertise, we can develop a compelling narrative to help you achieve your desired outcomes - whether that be lobbying policy change, building a case for investment or demonstrating the impacts of your business on the economy, on society and on the environment.

Read the CBI Economics insights for the latest examples of our work.

Get in touch today to find out more about economic consultancy from CBI experts.